No post this weekend b/c I was at the beach with the fam.

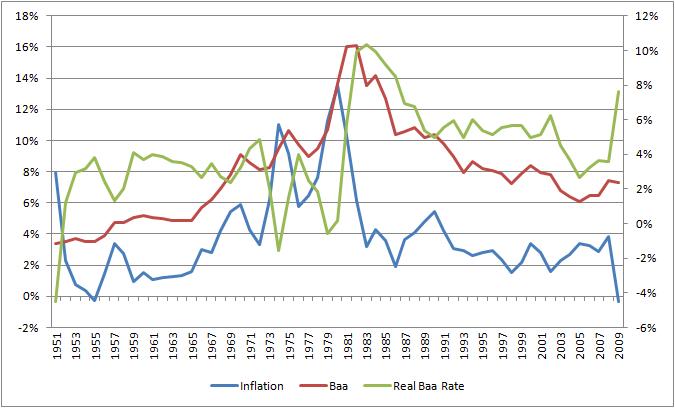

I started out this day mowing the lawn and thinking about a nice recent post at Crossingwallstreet.com that has to do with the outlook for gold prices and asserts that a main driver thereof is real interest rates (i.e. nominal interest rates minus inflation). Naturally, I wondered about the relationship (if any) between real interest rates and the stock market. My hypothesis was that an inverse relationship exists such that the stock market suffers when companies' cost of capital (real interest rate) increases. I'm interested in this potential relationship because I tend to think real interest rates will generally trend higher in the intermediate term as the Federal Reserve is forced to eventually confront inflation pressures by raising short-term rates / soaking up some of the base money supply. I'm not saying inflation pressures exist at present, I'm just inclined to think they are poised to increase over time as lenders and borrowers each become healthy enough to lend and borrow again, thus increasing the velocity of money (i.e. effective money supply).

I started out this day mowing the lawn and thinking about a nice recent post at Crossingwallstreet.com that has to do with the outlook for gold prices and asserts that a main driver thereof is real interest rates (i.e. nominal interest rates minus inflation). Naturally, I wondered about the relationship (if any) between real interest rates and the stock market. My hypothesis was that an inverse relationship exists such that the stock market suffers when companies' cost of capital (real interest rate) increases. I'm interested in this potential relationship because I tend to think real interest rates will generally trend higher in the intermediate term as the Federal Reserve is forced to eventually confront inflation pressures by raising short-term rates / soaking up some of the base money supply. I'm not saying inflation pressures exist at present, I'm just inclined to think they are poised to increase over time as lenders and borrowers each become healthy enough to lend and borrow again, thus increasing the velocity of money (i.e. effective money supply).

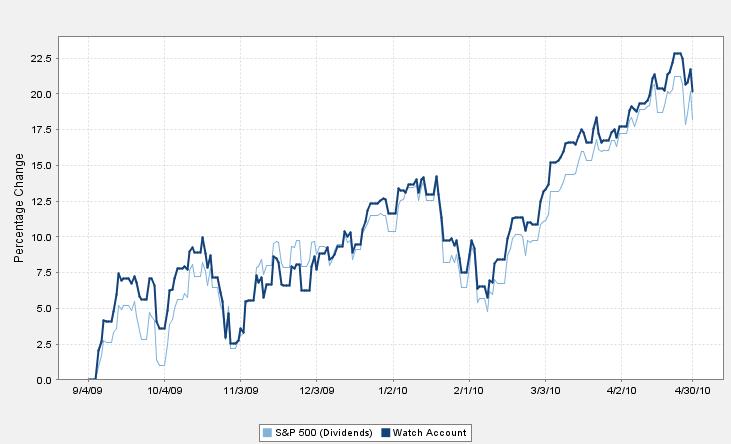

In a further effort to decrease correlation with the S&P 500, I've decided to allocate 1/3 of the model portfolio to foreign stocks with low betas. The new holdings will be 'acquired' tommorow via commission free trades and are shown in the chart above (32 stocks and 2 ETFs). Note: click the charts twice to enlarge them further for easier viewing.

In a further effort to decrease correlation with the S&P 500, I've decided to allocate 1/3 of the model portfolio to foreign stocks with low betas. The new holdings will be 'acquired' tommorow via commission free trades and are shown in the chart above (32 stocks and 2 ETFs). Note: click the charts twice to enlarge them further for easier viewing..jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)