A trading book I was reading a few weeks ago had a chapter on

Martingales and Anti-Martingales. I already knew the pitfalls of a Martingale strategy based on an unfortunate occurrence in Vegas a few years ago when I had but 15 minutes before needing to catch a cab to catch a red eye back to home. I sat down at a $10 black jack table with a couple friends and proceeded to double my bet every time I lost hoping the ever present risk of a run of bad hands wouldn't be realized. I was $800 lighter in the pocket when I caught that cab.

Anyhow, when reading of the Anti-Martingales strategy whereby one increases their bet after a win and decreases the bet after a loss, I was reminded of the book

Bringing Down the House wherein this type of strategy was used for risk management purposes. So the combination of these two experiences created a desire to back-test the strategy against historical stock market data (SURPRISE!).

Using Dow Jones Index data from yahoo! finance going back to 1929, I ran the following test:

1. If the prior day was a down day, then don't invest.

2. If the prior day was an up day, then invest 100%.

3. If the prior two days were up, then invest 200%.

4. If the prior three or more days were up, then invest 300%.

Historically speaking, this strategy would have needed to use margin (i.e. borrowed money) to purchase stocks equal to 200% or 300% of ones bankroll or 'stake'. However, today such leverage can be effectuated via ETFs such as

UPRO and

SDS.

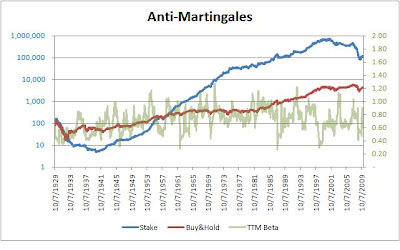

The results of the test are displayed in the charts above. Some interesting take-aways:

1. The Anti-martingales strategy produced higher returns than the Buy&Hold strategy whilst its Beta (relative to the Buy&Hold strategy) typically ranged over time from 0.5x to 1.0x, thus producing a considerable amount of Alpha when measured over the entire 80 years.

2. There were a couple time periods, such as the 1930s and 2000s, when the Anti-martingales strategy would have cost someone ~90% of their stake.

3. All the outperformance of the Anti-martingales strategy came from the period 1940-1974. From 1974 to 2000ish, the returns of Anti-martingales essentially matched those of the Buy&Hold strategy.

4. Around 1974, the average 'run' of either positive or negative days in the market experienced a sudden drop from ~2.3 days down to ~1.9 days. Although I'm not sure why the average 'run' suddenly decreased then (widespread use of computers for trading?), the fact that it did obviously impacted the performance of the Anti-martingales strategy.

Conclusion: I wouldn't try this Anti-martingales strategy since it hasn't worked since 1974. However, the last time this strategy experienced a 90% decline (1930s), it really outperformed over the subsequent 35 years. Perhaps since this strategy experienced a 90% decline in the 2000s it could be poised for some outperformance.